What Most Veterans Don’t Know About Their VA Home Loan Benefit

Buyer

Buyer

For many Veterans and active-duty military families, homeownership can feel financially overwhelming in today’s housing market.

Higher home prices, mortgage rates, and upfront costs often cause buyers to pause and wonder whether purchasing a home is even realistic right now.

But many Veterans may be much closer to homeownership than they realize.

The reason?

A large number of eligible buyers still do not fully understand the true advantages available through the VA home loan program.

And those benefits can be extremely powerful.

The VA home loan program has helped military families achieve homeownership for more than 80 years.

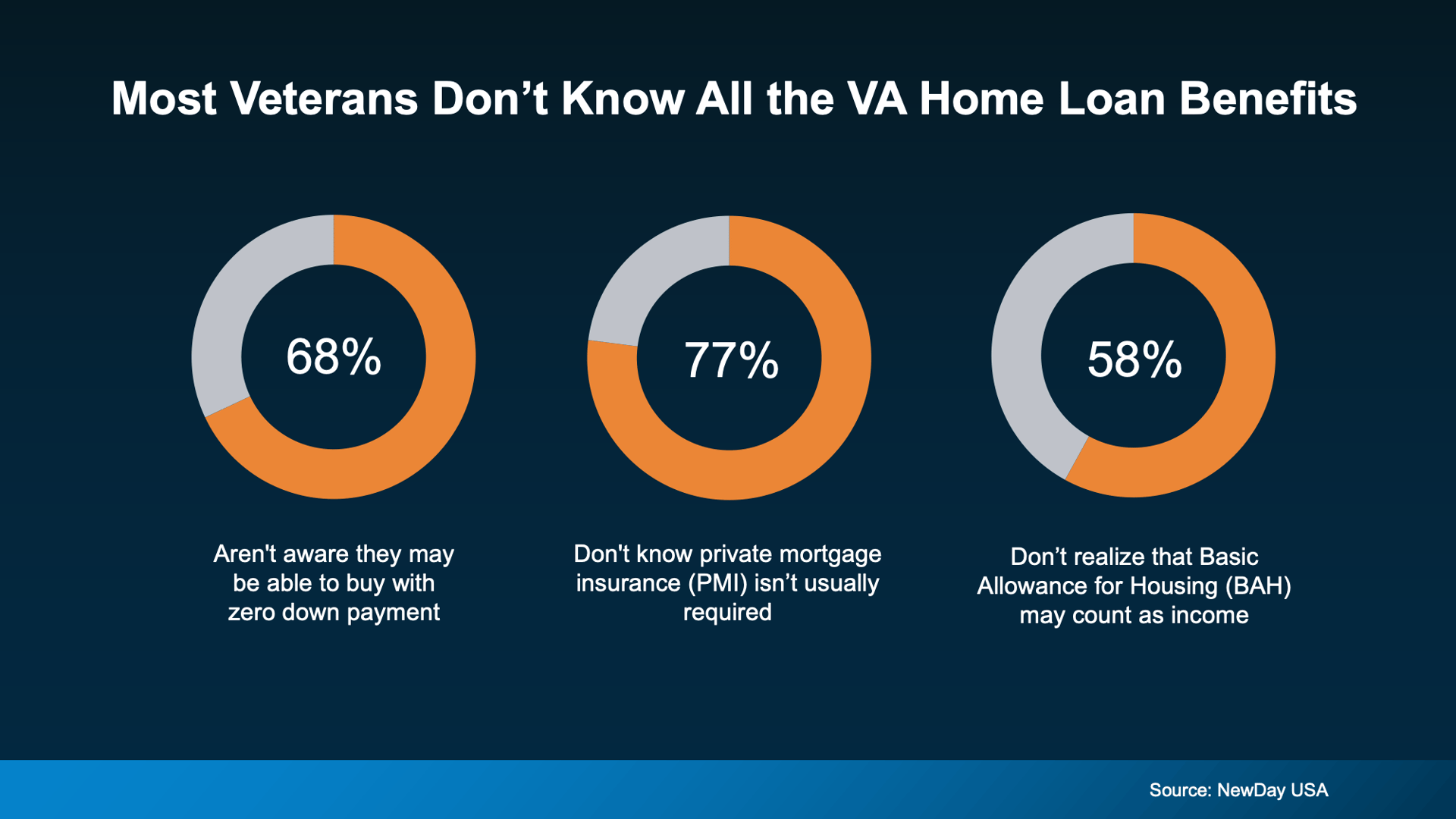

Yet according to a recent NewDay USA survey, many Veterans remain unaware of several major advantages available to them (see graph below):

Some of the most common misconceptions include:

Unfortunately, these misunderstandings may delay homeownership unnecessarily.

One of the biggest benefits of many VA loans is the ability for qualified buyers to purchase with zero down payment.

That can dramatically reduce the upfront cash needed to buy a home.

According to the survey, many Veterans believed they needed to save between $10,000 and $20,000 before purchasing a home.

For some eligible buyers, that may not be necessary.

This feature alone can significantly shorten the timeline to homeownership.

Another major advantage:

VA loans typically do not require private mortgage insurance (PMI).

Many conventional loans require PMI when buyers put down less than 20%.

That additional monthly expense can often range from hundreds of dollars per month depending on loan size.

Over time, eliminating PMI may save buyers thousands of dollars.

The Department of Veterans Affairs also places limits on certain closing costs that Veterans may be charged.

That can potentially reduce the amount of money needed at closing and improve overall affordability.

Combined with little or no down payment requirements, this may create meaningful financial flexibility for buyers.

For active-duty military members and qualifying reservists, Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may also help with loan qualification.

Because these benefits are generally non-taxable, they may increase purchasing power and help buyers qualify for more than they initially expected.

While VA loans offer tremendous advantages, every buyer’s financial situation is different.

That’s why working with knowledgeable professionals matters.

An experienced lender familiar with VA financing can help explain:

✔ eligibility requirements

✔ financing options

✔ monthly payment expectations

✔ closing cost structures

✔ and overall purchasing power

And having the right real estate strategy is equally important — especially in today’s competitive housing market.

Many Veterans have earned access to one of the most valuable home financing opportunities available today.

Yet countless military families still underestimate how powerful those benefits may be.

If you’re active duty, a Veteran, a reservist, or know someone who may benefit from VA financing, understanding your options could open the door to homeownership much sooner than expected.

And if you’re considering buying in New Jersey and want trusted guidance navigating the process strategically, I’d be honored to help.

Warmly,

Lan Ficarra

GOLDORIA GROUP | Brokered by eXp Realty

📲 908-463-2147

Buyer

Buyer

General

General

General

General

General

Buyer

Buyer